com LLC makes no representations or warranties of any kind, reveal or suggested, regarding the operation of this site or to the info, material, products, or products consisted of on this site. You expressly agree that your use of this site is at your sole threat.

One of the biggest impacts on your property owners insurance coverage cost is where you live. If you reside in an area susceptible to typhoons or earthquakes, for example, you generally will need additional protection which will likely impact your rate. In addition to your region, the physical area of your house matters, too. Being close to a police or fire station are contributing aspects, in addition to living in a neighborhood that experiences a high number of thefts. Keep in mind, trustworthy house owners insurance shouldn't need to strain your budget plan. There are a lot of opportunities to conserve, such as bundling your automobile and homeowners policies.

Requirement property owners policies provide coverage for disasters such as damage due to fire, lightning, hail and surges. Those who reside in areas where there is threat of flood or earthquake will require protection for those catastrophes, as well (What is mortgage insurance). In every case, you'll desire the limitations on your policy to be high enough to cover the cost of rebuilding your house. The price you spent for your homeor the current market pricemay be basically than the expense to reconstruct. And if the limit of your insurance coverage policy is based on your home loan (as some banks need), exit timeshare now it may not properly cover the cost of restoring.

To make certain your house has the correct amount of structural protection, think about: Regional building and construction expenses The square footage of the structure For a quick price quote of the amount of insurance you need, increase the total square video of your home by local, per-square-foot building expenses. (Note that the land is not factored into rebuilding estimates.) To learn building costs in your community, call your regional property representative, home builders association or insurance agent. The type of exterior wall constructionframe, masonry (brick or stone) or veneer The style of your house, for example, ranch or colonial The number of bathrooms and other spaces The kind of roof and materials utilized Other structures on the properties such as garages, sheds Unique features such as fireplaces, outside trim or arched windows Whether the houseor a part of itwas customized built Improvements you have actually made that have added value to your home, such as the addition of second bathroom, or a cooking area remodelling Structure codes are updated occasionally and might have changed significantly considering that your house was developed.

If you believe that aspects of your house are not up to current building regulations, consider getting a recommendation to your policy called an Ordinance or Law, which pays a defined amount towards bringing a house up to code during a covered repair work. Beautiful, special functions on older homeslike wall and ceiling moldings and carvingsare pricey to recreate and some insurer may not provide replacement policies because of that. If you own an older home, you may have to purchase a customized replacement expense policy. This means that instead of fixing or changing functions typical of older homeslike plaster wallswith like materials, the policy will pay for repairs using today's basic building materials and building and construction techniques.

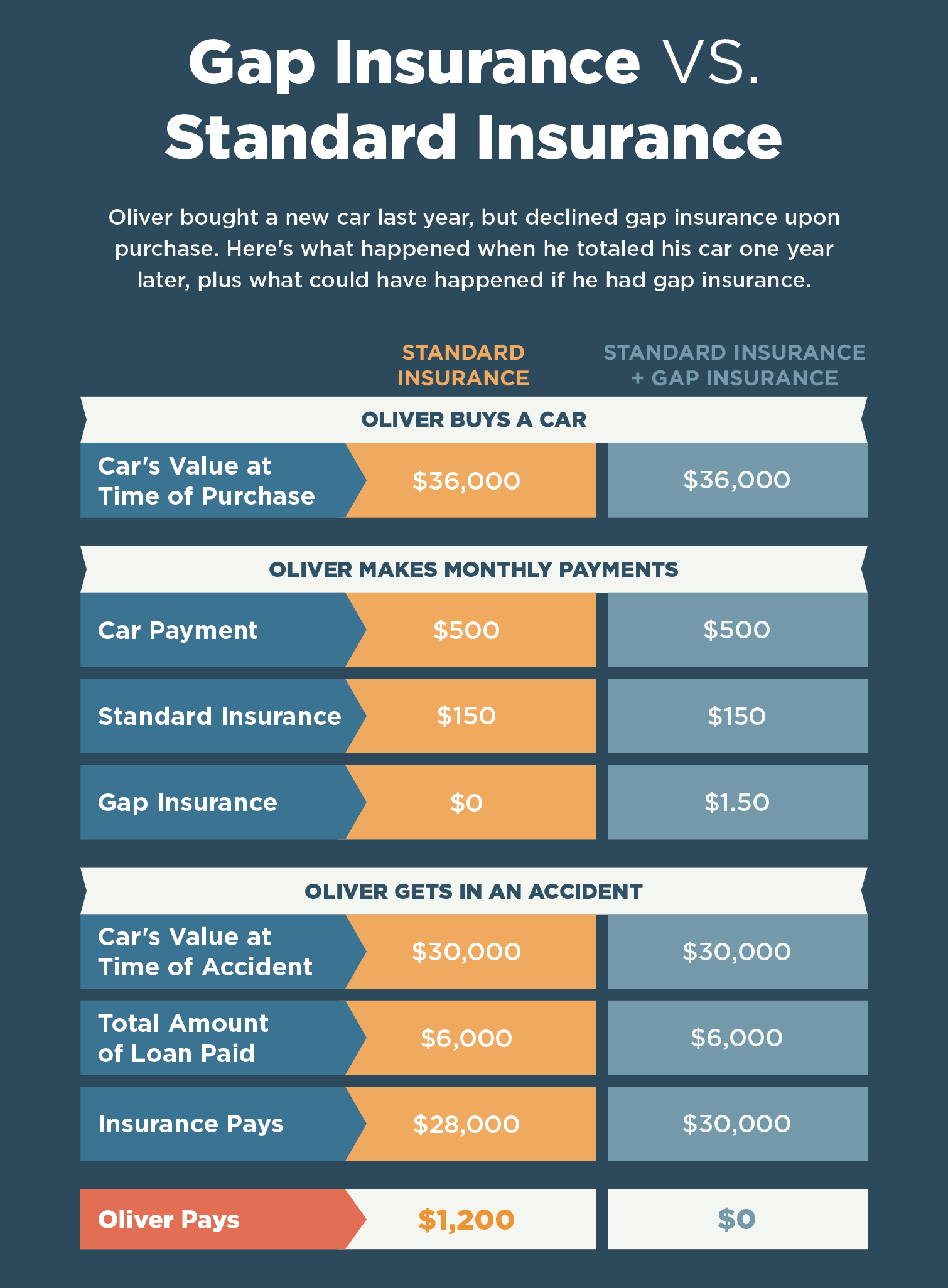

See This Report about How Much Is Title Insurance

If you plan on owning your house for a while, consider including an inflation guard clause to your policy. An inflation how to terminate a timeshare guard instantly adjusts the dwelling limit to reflect current construction costs in your location when you renew your insurance coverage. After a significant catastrophe such as a typhoon or tornado, building costs may rise unexpectedly due to the fact https://zenwriting.net/fordusfqu3/drivers-with-bad-credit-pay-a-rate-that-is-71-greater-on-typical-than-a that the cost of building products and construction workers increase due to the widespread demand. This price bump may press rebuilding costs above your house owners policy limitations and leave you short. To safeguard against this possibility, a guaranteed replacement expense policy will pay whatever it costs to restore your house as it was before the disaster.

Many property owners insurance plan supply protection for your personal belongings at about 50 to 70 percent of the insurance on your residence. Nevertheless, that standard amount may or may not suffice. To find out if you have enough coverage: In order to accurately assess the worth of what you own, it's highly a good idea to perform a home stock. An in-depth list of your belongings will not only help you find out how much insurance you need, but it will likewise work as a convenient record. In the event any or all of your stuff is taken or damaged by a disaster a stock will make filing a claim much easier.

While you're reviewing your belongings, think of whether you desire to guarantee them for real cash worth (where the policy would pay less money for older products than you spent for them new) or for replacement cost (which would cover to change the items). The price of replacement cost coverage for homeowners is about 10 percent more but is usually a beneficial investment in the long run. (Keep in mind that flood insurance for valuables is just readily available on an actual cash worth basis.) If you think you require more coverage, contact your insurance coverage expert and inquire about higher limits for your personal possessions.

For instance, fashion jewelry coverage may be limited to under $2,000. Some insurance business might also position a limitation on what they will pay for computers. Check your policy (or ask your insurance coverage expert) for the limits of your coverage for any expensive products. If your house stock consists of items for which the limitations are too low, think about purchasing a special individual home floater or a recommendation. This will enable you to guarantee prized possessions individually or as a collection, with significantly higher protection limits. Additional Living Expenses (ALE) is a really essential feature of a standard homeowners insurance policy. If you can't reside in your home due to a fire, extreme storm or other insured disaster, ALE pays the additional expenses of momentarily living somewhere else.

If you lease part of your home, this coverage likewise reimburses you for the rent that you would have gathered from your occupant if your home had not been ruined. Lots of policies offer protection for about 20 percent of the insurance coverage on your house. However ALE protection limits vary from company to business. For instance, there are policies that offer a limitless quantity of protection, for a limited quantity of time, while others may just set limitations on the amount of coverage. Most of the times, you can increase ALE protection for an additional premium. The liability portion of homeowners insurance coverage covers you versus suits for bodily injury or home damage that you or relative or animals cause to other individuals, in addition to court expenses incurred and damages granted.